Daily Insights Report 13/04/17

- 13 Apr 2017

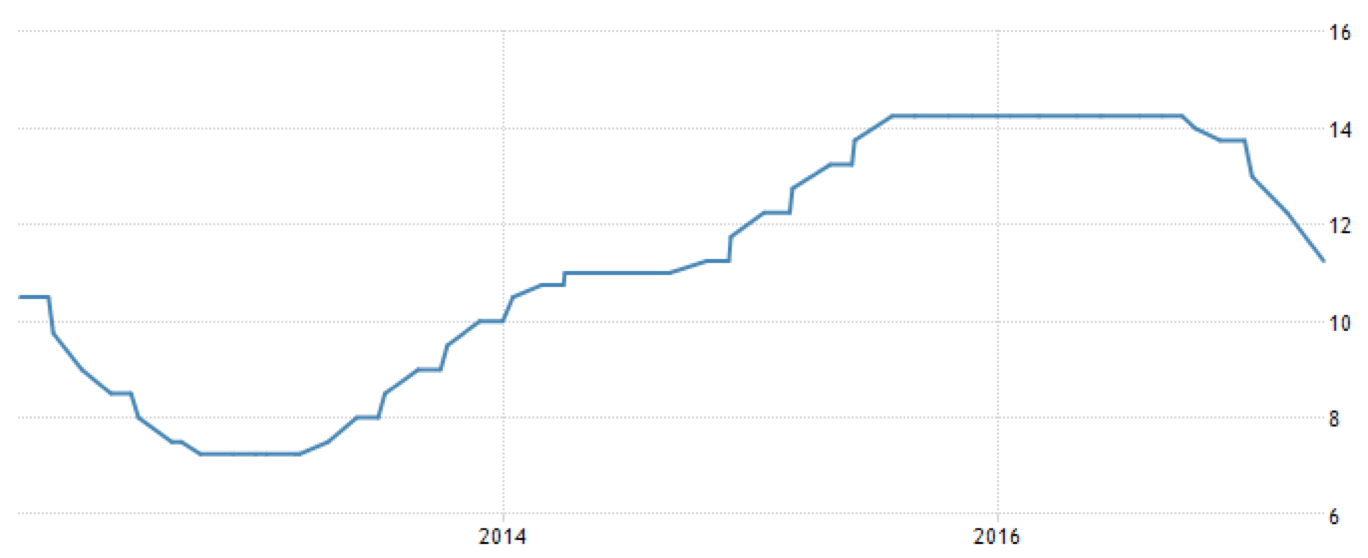

The Central Bank of Brazil cut its key Selic rate by 100 bps to 11.25% on April 12, while this is what markets had predicted, it is important to understand the trend being seen in the country. It is the fifth straight decline, and borrowing costs now match a low level that was seen in November 2014. This can be seen in the chart below.

– President Trump comments of stating that the Dollar ‘was getting too strong’ led to a late sell-off of the currency. He stated that he would prefer for the Federal Reserve to keep interest rates low. Following that, he made the announcement that he would not label China as a currency manipulator. As a result of this, the Dollar was down 0.3% against the Yen at a five-month low of 109.23 as the President’s remarks gave the traditionally safe haven currency upward momentum. US Treasuries benefitted from this risk-averse tone with the yield down 2.26%.

– The Euro was up 0.5% against the Dollar to reach 1.0654, but was little changed against the Yen which was trading at 116.30. Developments in the French election will likely be a determining factor for the price of the Euro. One scenario is that if we get more information about Marine Le Pen gaining ahead of the polls on April 23, it is likely that people will sell Euros.

– The Yen has recently almost dominated the CHF in being named a safe haven currency. This is because the Swiss National Bank intervened with an amount of 67 B CHF in 2016, at times of uncertainty.

Commodities

– Oil prices showed to have a choppy session as profit-taking emerged after a six-day rally for Brent crude as participants digested the latest data about US inventories. Brent crude settled at $55.86 a barrel, down 0.7% after earlier reaching $56.65 – the highest level seen in five weeks.

– Due to the Dollar’s retreat in the last half an hour of trading yesterday, it helped push gold up by $8, which is the equivalent of 0.6% to reach $1,281 an ounce.

United States Dollar (USD)

Jobless claims (week ending April 8)

Forecast for this data is 255,000 initial claims. This is a rise from the previous week from 234,000. An increase in initial claims is likely but they are volatile around holidays and the incoming data is for the week before Good Friday. The trend in initial claims should be between 250,000 and 260,000. The trend earlier this year was likely slightly depressed because of the weather situation.

Euro (EUR)

Germany – Consumer Price Index (March)

Preliminary estimates show that Germany’s consumer prices rose by 1.6% year-over-year in March, slowing down from February which saw a 2.2% increase. The 2.2% increase was the fastest increase seen in Germany since August 2012.

Inflation coming from energy and food prices eased slightly. Energy prices rose 5.1% year-over-year after rising 7.2% in February. Growth of food prices slowed to 2.3% year-over-year from 4.4% previously seen. The growth of prices of services has almost halved to 0.7% from 1.3% in February. This price pressure comes mainly from higher commodity prices, so it should not be confused with an increase in demand. The relatively weak Euro has also been supporting inflation pressures in recent times. Higher prices for oils and metal pushed input prices higher for German producers, as Markit manufacturing PMI has reached an almost six-year high.

France Consumer Price Index (March)

France’s annual harmonized consumer prices likely rose 1.1% in March, which is slightly down from February. The annual number has decelerated due to lower prices of manufactured goods, while the prices of services remained strong. Annual prices of tobacco added close to 3.0% in March and the prices of Energy rose nearly 10%. Core inflation has already stayed in the positive area. It is likely that inflation will strengthen in the coming months, as there will demand-pull and cost-push inflation. Therefore, the inflation target should be reached within about half a year.