Daily Insights Report 20/02/17

- 31 Mar 2017

20 Feb 2017

Markets in the US will be shut on Monday in Observance of President’s Day.

UK Retail sales fell by 0.3% month-over-month in January 2017. This comes after a 2.1% drop in December and misses the expectations of the 0.9% gain. While many industries contributed to the decline, the biggest loser was non-store retail, petrol stations, and food stores. On an aggregate, sales did rise, by 1.5%. This is their weakest performance since November 2013.

At the end of last weeks trading session, the S&P500 closed at a record high. This comes after a 10% rally in the stock of Kraft Heinz. The general sentiment with investors remained cautious, as this might be the week that the new tax plan is released. The Yen also continued its rally against the USD and ended the week at 112.90 after reaching 113.3 on Tuesday.

The week ended with generally stronger than expected economic data. Inflation, retail sales and regional manufacturing all beat forecasts, and gave the Dollar small rallies along the way. All the while, investors wait for Donald Trump to reveal his new tax policy.

An interesting idea to notice was that the impact of announcements by the Federal Reserve are no longer as strong as they used to be. This is likely because the power of the new presidential administration has highlighted the importance of trade and fiscal policies back into the spotlight. Interest rates changes in the US may eventually become a lagging change to the indicator for the economy itself, rather than a steering factor.

The Euro last week had not performed well. Likely due to a few factors:

1 – The week of economic data from the region disappointed investors, especially data considering the regions manufacturing output.

2 – The French election is coming closer. And the uncertainty of which direction financial markets might move as a result of the end result are unsure. Since France plays such an important role in the EU, It is worthy of adding this level of precaution.

3 – Bailouts provided by the ECB for Greece are not likely to go away, but this is not confirmed.

As a result of these, the Euro ended at $1.0609.

The Pound also showed to weaken by the end of the week. This comes after data showed retail sales declining. The Pound ended at $1.24.

Commodities

– Oil prices ended the week on a stronger note. During the week, oil saw a lot of volatility. Brent crude oil settled with a 0.3 increase by the end of the week at $55.81. West Texas Intermediate (WTI) crude on the other hand ended at $53.38. Many traders will be paying special attention to the Brent this week. This is because the major oil pricing agencies are set to decide whether or not they will keep Brent crude as a benchmark for the global oil purpose. There is a proposal to replace the benchmark of North Sea Brent with Troll. This would come from Norway’s Statoil Corporation. In the short run, if Brent is removed from a benchmark, it would give WTI all the spotlight. While just a decision may come this week to remove Brent, the actual change will come after many years, but a gradual shift would begin almost immediately.

– Gold ended the week with a slight decline and was trading at $1,235 per ounce on the spot market.

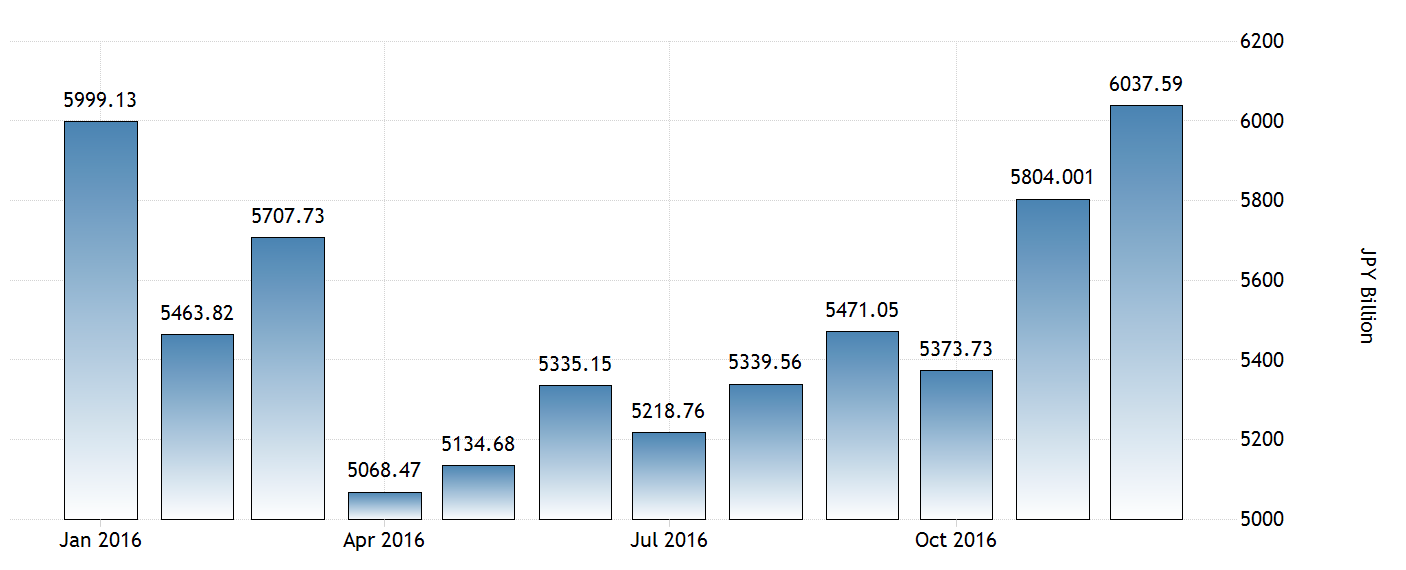

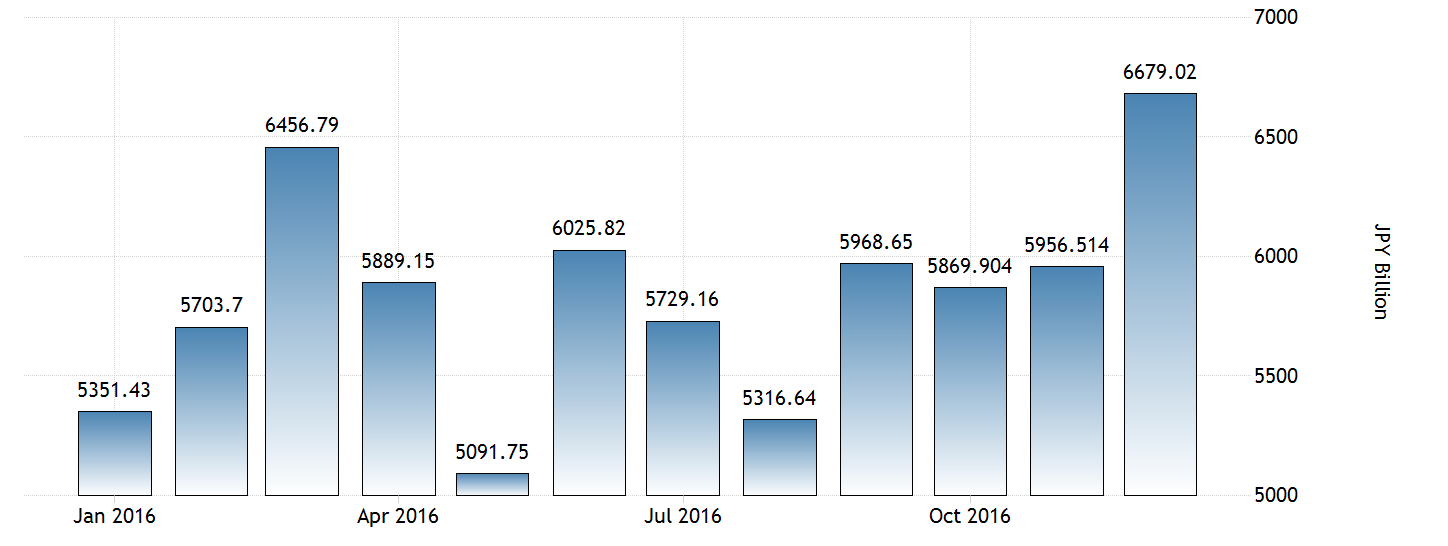

Japanese Yen (JPY)

Foreign Trade (January)

Exports in Japan likely increased in the month of January because of the overall Yen that has weakened. While the currency continues to depreciate, it grows in international competitiveness and will be more attractive in the global marketplace. Looking at the chart below, we can see how exports have grown in recent times.

While this would be attractive if we looked at it alone, we should also pay attention to the overall trade balance. This balance likely stayed the same even though exports have shown growth. Imports likely increased as well since commodity prices have been increasing.