Daily Insights Report 04/04/17

- 4 Apr 2017

4 April 2017

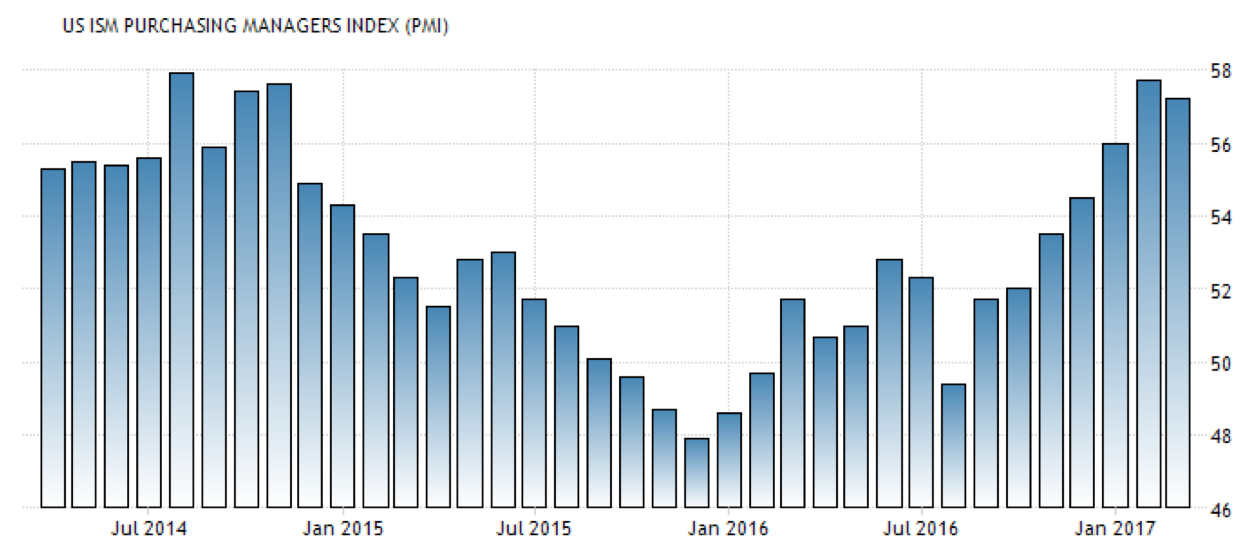

Data from US factory activity showed that growth was less than initially expected. The ISM Manufacturing PMI fell to 57.2 in March from a 30-month high of 57.7 that was shown in February’s data. New orders and production grew less while employment and export orders indexes showed to have jumps. How this data set has behaved in recent history can be seen in the chart below.

In China, the Caixin-Markit manufacturing PMI fell from 51.7 in February to 51.2. While this shows a slight decline, it is the ninth consecutive reading above the 50.0 level which is normally the dividing line between contraction and expansion.

It has been reported that more than one million people have been lifted out of unemployment in the Euro zone during the past year, pushing the jobless rate to the lowest in almost eight years. Factories in the Euro Zone also enjoyed growth, some showing their highest levels of activity since 2011. Factories in Italy showed to be their busiest in five years.

– The AUD showed to take a small fall after data showed that retail sales in the country had shrunk 0.1% month-over-month in February, from a 0.4% growth in the previous month which had beaten expectations. The AUD fell to USD 0.7603.

Commodities

– Energy stocks came under renewed pressure after oil prices fell back. Brent crude settled at $53.12 a barrel, showing a decrease of 0.8%. At the same time, West Texas Intermediate (WTI) crude was down by 0.7% to reach $50.27 a barrel.

– Since the Dollar showed slight weakness with the new trend, this gave support to the price of gold. Gold rose $4 to reach $1,2533 an ounce.

Euro (EUR)

Retail Sales (February)

Euro zone retail sales are likely to have increased by 0.5% month-over-month in February after reversing the 0.1% decline seen in the previous month. Strong data from Germany were likely the main contributor to this uptick. Germany’s sales data was seen to have bounced up to 1.8% month-over-month in February from January’s 1.0% month-to-month increase. The picture was not as pleasant as Spain and Italy’s. Though Spain’s retail sales is likely performing better than Italy’s, Italy is likely to have shown that retail sales contracted. PMI from Italy shows that the headline index is at a five-month low at 45.5. Since this magnitude and direction of this data is not yet known, it could be a reason for the Euro Zone’s retail sales to be 0.4%.

United States Dollar (USD)

Trade Deficit (February)

The nominal trade deficit likely narrowed from 48.5B USD to 44B USD in February. The early Lunar New Year likely improved imports, but the effect should have subsided by February’s data. The forecast assumes that the service industry’s surplus improved slightly in February. The nominal trade deficit has been averaging at 46.2 B USD per month, which is higher than the 44.1B USD average seen in the fourth quarter of last year. It is likely that net exports will still be a slight drag on the first quarter of GDP growth.

Technical Analysis

GBPAUD

Looking at the daily chart of this currency pair, a hybrid of a symmetrical pattern and descending triangle can be seen. The pair seems to be approaching the corner of this triangle so a breakout may be due. The stochastic chart is moving upwards which suggests that the currency pair may go upwards.

Recent data coming from Australia have not been so strong lately. This can be seen in retail and trade figures. The upcoming RBA interest rate announcement may not be as optimistic as in the past.